For many people, life insurance can provide a measure of financial security for their loved ones after they pass away. However, many decisions go into the process of purchasing life insurance, including how you make your premium payments.

Payment plans and life insurance premiums vary by provider and policy. Most providers allow you to pay monthly, semi-annually, quarterly, annually or in full. There’s flexibility in how often you pay your premiums, but the choice affects how much you’ll end up paying for coverage. Let’s look at the advantages of paying your policy in full, making annual payments, or monthly payments.

Paying Life Insurance Premiums Annually

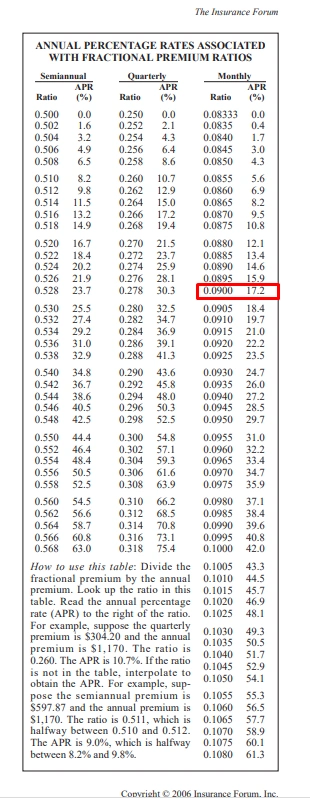

A significant benefit of choosing annual payments is cost savings, as you may be able to save up to potentially 30% by paying for your policy premium annually depending on the provider. Some insurance companies do not disclose the annual percentage rates (APRs) for policyholders. Don’t hesitate to ask your Experior Financial Group Associate for help in calculating the applicable annual percentage rate for your premium payment.

For example, if the monthly premium payment on the policy is $90.00 but the annual premium payment is $1000.00 by doing a simple calculation, you can determine the ratio would be 0.09. If we then take that percentage and view the chart below, which was created by The Insurance Forum, you’ll see that you can save approximately 17.2% if you pay this premium annually compared to monthly. This is a major cost savings that you’ll want to take into account when deciding on payment terms for your policy.

By paying for your life insurance policy annually rather than monthly, you will save money on your premium and free up extra money each month that can be better spent paying off debt or investing for retirement. Pay your premium in full once per year, and you can put it out of your mind for the next 12 months.

Paying Life Insurance Premiums Monthly

The cost of a life insurance policy can vary from just a few hundred dollars to thousands of dollars, based on your age, health, and whether you choose permanent or term life insurance. If you can’t afford to pay the full premium fee all at once, making monthly payments may be a good option for you.

Making monthly premium payments lets you pay for life insurance month by month, like you would any other bill. When you have life insurance as part of your budget, it can be easier to save money. Payment of monthly premiums may give you liquidity and allow you to build up a nest egg that is more flexible than the permanent life insurance policy you might be considering.

Is It Possible To Completely Pay Off A Whole Life Policy?

- Premium payments – Once the policy owner has made enough premium payments, the policy will reach its paid-up status.

- Reduce Feature – Your whole life policy can be made paid-up by taking advantage of the reduce feature.

Regardless of which method you choose, the policy remains in force and premiums are eliminated. It offers numerous benefits as well. One of the biggest advantages is that it covers you for your entire life. Additionally, you can build up tax-deferred savings for the length of the policy.

How Paid-Up Life Insurance Policies Work

There are two kinds of paid-up insurance: paid-up status and paid-up additions. Paid-up life insurance can be a smart financial move. With paid-up status, you continue to have your policy in force without having to continue paying premiums. If you were to pass away, your beneficiary would receive the death benefit.

Paid-up additions are essentially miniature life insurance policies, where your cash value will accumulate through your premium payments. If, for instance, you pay 10 dollars, that 10 dollars will be added to your policy as cash value. Additionally, dividends earned by a whole-life policy are used to buy additional coverage, adding to your cash value. The policy is paid up, which means it doesn’t require any further financial commitment.

Converting Your Insurance Policy to Paid-up Status

You can keep your coverage in place without paying premiums, depending on the specifics of your policy. However, you should look at the details of your policy, as this option may not be available with every insurance company. If you decide to convert to a paid-up status, it means you no longer have to make premium payments moving forward. Premiums are deducted from your cash value account, which keeps your policy in effect.

That means that, depending on your policy’s guidelines, you may be able to end temporary or permanent payments altogether. Your death benefit could also decrease. If you die before your premiums are paid, your beneficiary will only receive the amount not yet paid on your policy.

Why Should You Consult With An Experior Financial Associate?

If you’re a savvy investor, you know that your life insurance policy is one of many options when it comes to planning your financial future. If you’re new to financial planning and investing, then you may need someone to help guide you through the process. When considering purchasing a life insurance policy, it is important to consider the return on your investment. Our Associates are experienced and willing to help you take the right steps to achieve your financial freedom. Experior’s client solutions are built around our proprietary Expert Financial Analysis software (EFA). It offers a simple, easy-to-follow financial program exclusively through Experior Associates. When you meet with an Experior Associate, they will complete a free, no-obligation Expert Financial Analysis. This customized financial plan will help the Experior Associate determine the right life insurance policy and premium payment method for you.

FAQ

If you want to keep your life insurance policy in force but can no longer afford to make premium payments, you may want to consider converting to paid-up status. Even if something unfortunate occurs, your beneficiaries will still receive at least some of your life insurance benefits.

But keep in mind, If you stop paying premiums, there are two things that will happen. First, the death benefit will be reduced. Second, if you need to borrow money or surrender the policy, some of its cash value will be lost.

Whole life insurance policies are different from term insurance. While term policies expire, whole life policies will stay in effect until you pass away or until the policy is canceled. Over time, the premiums you pay into the policy start to generate cash value, which can be used under certain conditions. Or if you opt for a Whole Life policy, you pay the premiums for a specified period of time, after that, the policy is considered paid up.

Individuals who have accumulated enough wealth to take care of their family upon their passing may not need to purchase life insurance. However, it’s important for couples and families to consider life insurance as a way to protect their loved ones’ futures and ease the expenses incurred should the insured pass away prematurely.

Whole life insurance policies are designed to provide a death benefit for beneficiaries in exchange for premiums. A whole life policy, unlike term insurance, is designed to pay benefits over the policyholder’s lifetime. Therefore, whole life insurance premiums do not increase as you get older.

- Cash out the policy

Under these circumstances, you can cancel your policy and begin to collect the available cash surrender value. At the same time, you will no longer be covered by life insurance.

- Non-forfeiture options

You might be able to buy a policy with a reduced death benefit and no cash saving, that allows you to stop paying premiums completely. If you have a cash value in your permanent policy, you may want to consider converting it to an extended term policy.

- Policy will lapse

If this happens, try asking your insurer if the policy can be reinstated. In some cases, your insurer may reinstate the policy if it has been lapsed for less than five years.

The best thing to do in all cases is have a licensed professional look over your policy and make sure you have the right product for you and your loved ones. This will give you peace of mind and is at no cost to you.